How Options Speculation Contributed to the Recent Market Correction

In the three days since hitting an all-time high last Wednesday, the Nasdaq (QQQ) lost 12.3% over the following three; the quickest 10%-plus correction on record. Today indices are rebounding. However, investors are wondering if this is merely a reflex rally within the start of a larger down move, and also what drove the relentless, and seemingly irrational 65% tear-up in the past few months.

There were several initial explanations for the rapid stock recovery, which included the massive monetary and fiscal stimulus, and the market cap weighting of the indices, in which Apple (AAPL), Microsoft (MSFT), and Amazon (AMZN) accounted for a disproportionate amount of the gains.

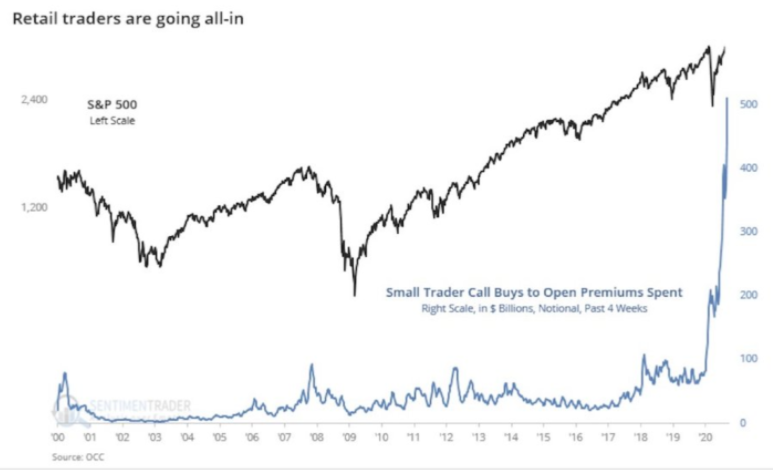

Another explanation was the surprising realization that many companies were actually benefiting from the pandemic-related behavior shift, which included tech companies such as ZOOM (ZM), and also sectors such as housing and old-line consumer staples. There is also the notion that younger people who had never invested or traded before, AKA Robinhooders, are fueling the speculation that was creating a bubble similar to 2000’s dot.com days.

Finally, as I wrote on Friday, the latest entry into options trading in the form of speculative call buying was the late August thrust in tech shares. More specifically, mainstream media focused on how Softbank (SFTBY), the giant Japanese investment fund that fueled the venture capital bubble epitomized by the WeWork (WE) debacle, had been pumping $4 billion dollars into tech options such as AAPL, AMZN, and DOCU. This created an outsized and in some ways artificial, demand that drove prices parabolically higher. It’s this last item I want to drill down into today, specifically the dynamics of how call-buying can become a “wag the dog” phenomenon, leading to price acceleration. This leads me to the conclusion that it was actually small Robinhooders, not the giant Softbank, that was the catalyst to the August blow-off.

The first thing to understand is the market makers, who facilitate or take the other side of a trade. Market makers don’t want to have a directional bias or position. In order to stay delta neutral, they must buy shares to offset the calls they sold. This can lead to a feedback loop, much like a short squeeze, where more calls are bought and the higher prices go — and the more market makers must buy to get hedged.

[Labor Day Sale Extended] Claim your SPECIAL One-Month $19 Trial Offer to the Options360 Service

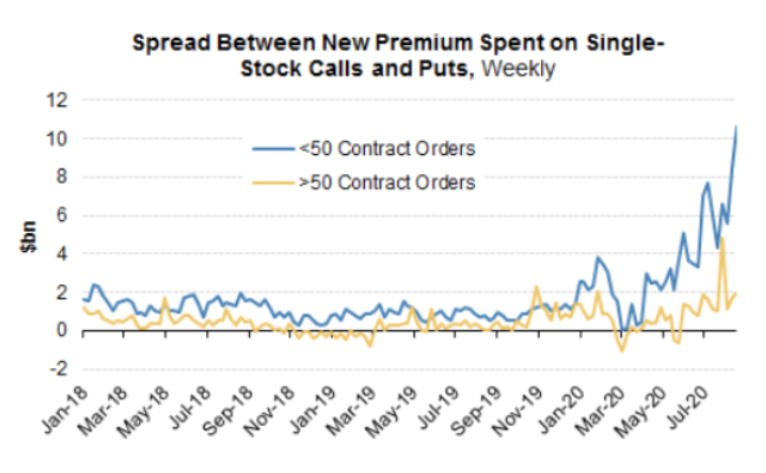

I’m going to walk you through an example in AMZN, demonstrating how this works, and to show you that it was retail speculation in short term call buying (“Robinhood”) and not institutional call spread trades in tech (SoftBank, etc) that drove the action. The Options Clearing Corp data shows small trader accounts (less than 50 contracts) bought $40 billion of premium in call options over the last month with a concentration on short-term duration (two weeks or less).

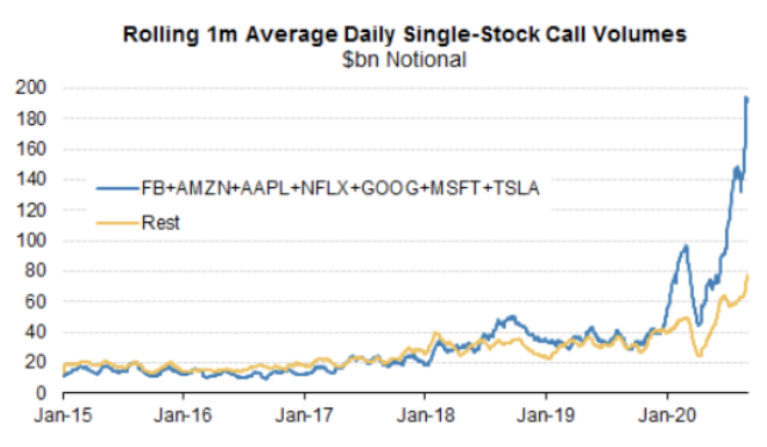

Also, most of this was focused on those big cap tech names such as AAPL, TSLA, AMZN, and NFLX.

The important thing to understand is that short term options have lots of leverage and gamma when the underlying price is near the strike. Meaning, the hedging requirements for a market maker to offset an outright sale of a short-term call is significantly more than offsetting a longer-term spread. Let’s get back to the AMZN example; A day trader who bought a one-week 3250 call with AMZN at $3148, on 8/14, would have paid about $15. The delta was 21%; the contract she bought is deliverable into 100 shares. So, it has the equivalent of 21 shares (or $66,100) worth of AMZN exposure, for only $1500 of premium. The market maker who she buys the call from is going to immediately hedge that exposure.

The next day, AMZN moved up 1.1% to 3182. As the stock moved closer to the option strike, the call price increased to $15.50 and its delta moved up to 26%. The market maker would have increased her hedge by buying another 5 shares, bringing it to 26 shares or $82,000 of stock. The day after AMZN moved up 4.1% to 3312, the call price exploded to $81 and delta to 73%. The market maker would have been forced to buy another 47 shares of stock, moving the total value of shares bought to $230,000. Remember: The day trader’s total premium outlay was $1,500.

This is how heavy buying of short-term options can accelerate moves in trending stocks. It turns a relatively small amount of option premium into a reinforcement mechanism: stock moves an option’s delta move higher which leads to market makers buying the stock for hedging purposes. By contrast, the purchase of longer-term calls, and even more so spreads, which is what institutional investors such as Softbank were engaged in, have much lower delta and gamma and therefore create much less buying or hedging pressure.

Data shows the bulk of call trading was by smaller accounts and in shorter-term options.

The thrust of all this is two-fold; options speculation certainly contributed to recent thrust tech share prices, and it was the near $40 billion in short-term retail speculation and not the $4 billion of Softbank that caused the bulk of the move. And in the current unwinding, it is those younger or newer traders that are learning the double-edged sword of options leverage.

CLICK HERE for a one-month trial with these trades and more to the Options360 Service for just $19!

The post How Options Speculation Contributed to the Recent Market Correction appeared first on Option Sensei.

(Want free training resources? Check our our training section for videos and tips!)