Bears Hold 50-Day Moving Averages

- The GDP numbers showed the first contraction of the economy in three years and marked the first quarter of negative growth since the start of 2022.

- After Wednesday’s close, a deal was announced between the United States and Ukraine over access to the country’s natural resources The new investment projects will help develop Ukraine’s natural resources including aluminum, graphite, oil and natural gas.

- The technical action remains slightly bullish despite yesterday’s mixed results as the 50-day moving averages for the major indexes remain in play. However, all remain in a downtrend and if they hold this week, it could be another indication of a near-term market top.

Wall Street traded on both sides of the ledger on Wednesday following an update on gross domestic product (GDP) that showed the economy contracted at an annual rate of 0.3% in the first quarter. The news weighed on the major indexes throughout the session before a late afternoon rally lifted the broader market and the blue-chips into positive territory.

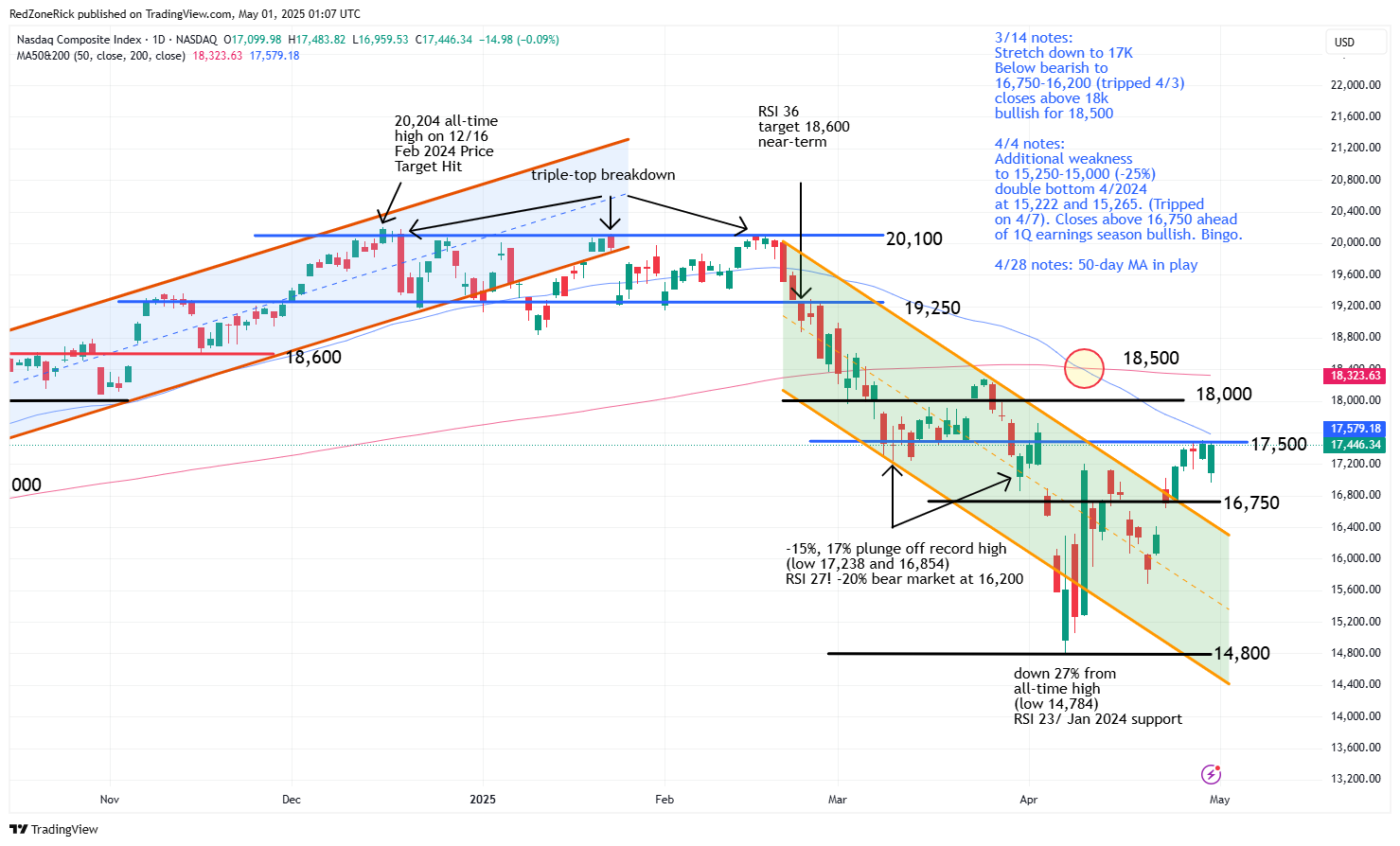

The Nasdaq tagged a low of 16,959 before ending at 17,446 (-0.1%). Key support at 17,000 held. Resistance remains at 17,500.

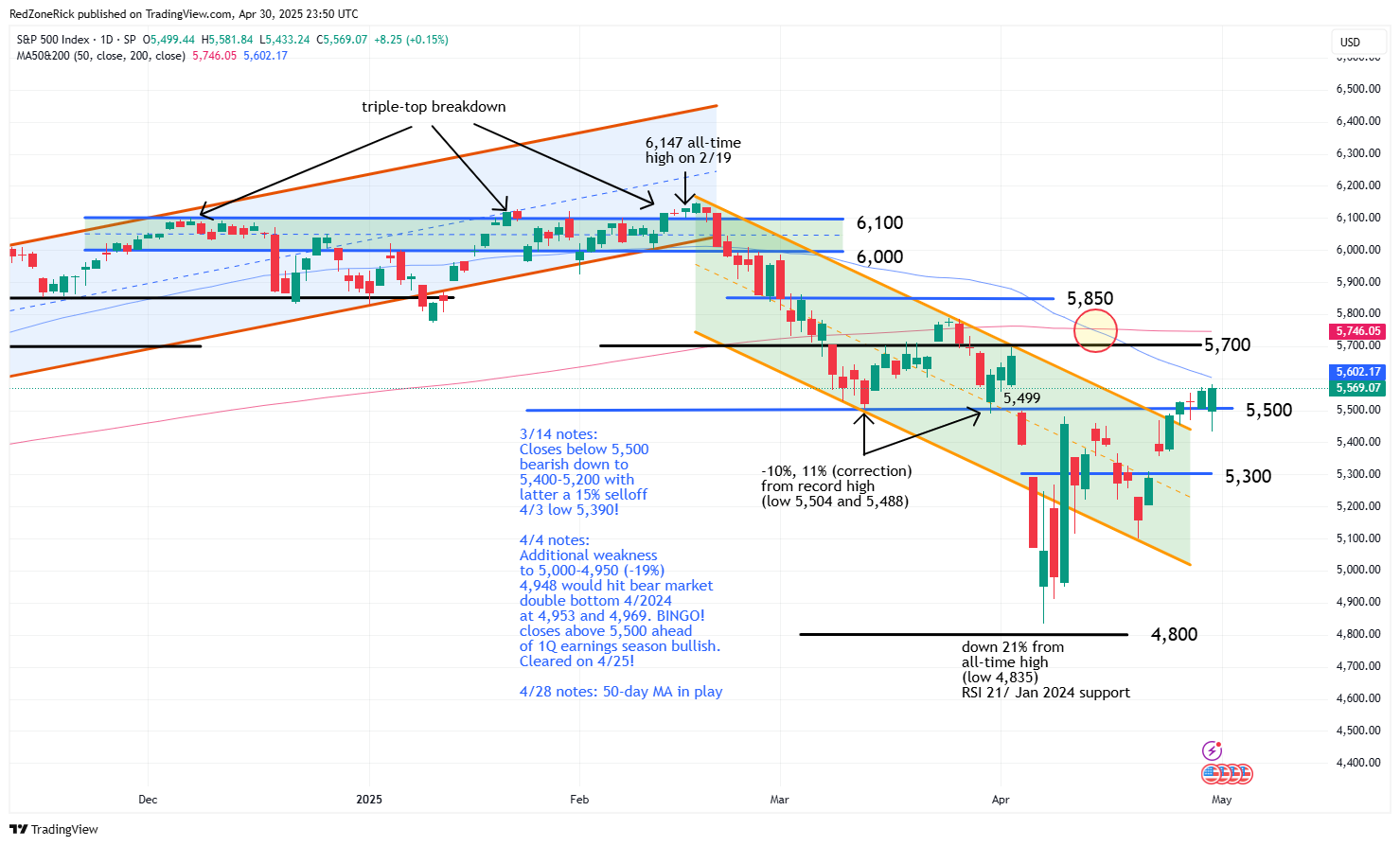

The S&P 500 went at 5,569 (+0.2%) after tagging a high of 5,581. Resistance at 5,600 held. Support is at 5,500.

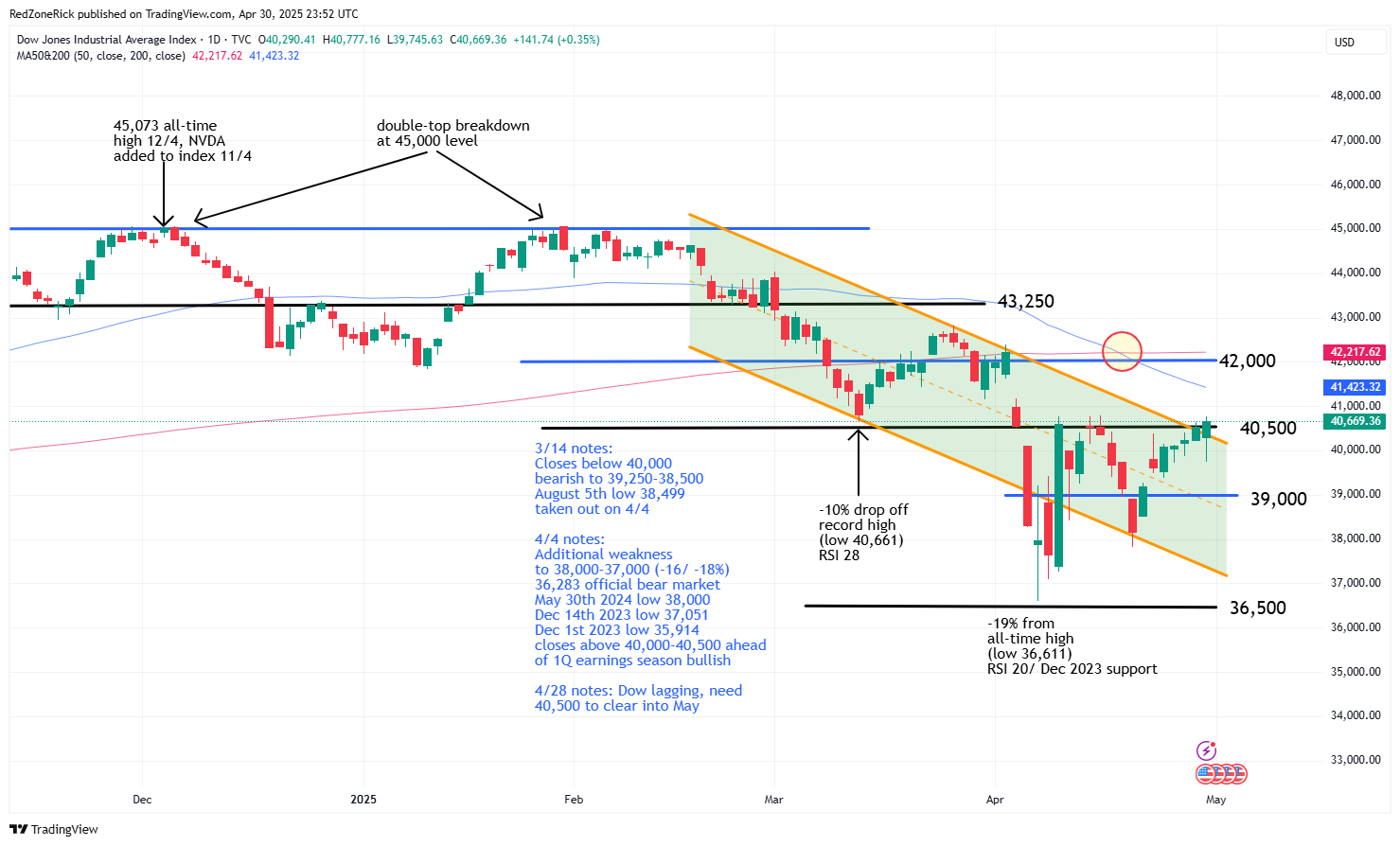

The Dow reached a peak of 40,777 while closing at 40,669 (+0.4%). Resistance at 40,750 held. Support is at 40,000.

Earnings and Economic News

Before the open: Eli Lilly (LLY), Roblox (RBLX), Mastercard (MA), McDonalds (MCD), Moderna (MRNA), SiriusXM (SIRI)

After the close: Airbnb (ABNB), Amazon.com (AMZN), Apple (AAPL), Roku (ROKU), Twilio (TWLO), US Steel (X)

Economic news:

Initial Jobless Claims – 8:30am

PMI Services Index – 9:45am

ISM Manufacturing Index – 10:00am

Construction Spending – 10:00am

Technical Outlook and Market Thoughts

The GDP numbers showed the first contraction of the economy in three years and marked the first quarter of negative growth since the start of 2022. A large surge in imports were to blame as companies advanced orders ahead of the anticipated tariffs. However, private investments picked up and offered a silver lining in the disappointing report.

The technical action remains slightly bullish despite yesterday’s mixed results as the 50-day moving averages for the major indexes remain in play. However, all remain in a downtrend and if they hold this week, it could be another indication of a near-term market top.

The Dow cleared and held key resistance at 40,500 on Tuesday and made a higher high on Wednesday. The next waves of resistance are at 41,000-41,500 and the 50-day moving average. The closes out of the downtrend channel were also a bullish signal.

Support is at 40,000-39,500 with yesterday’s low at 39,745 splitting the middle. A close below 39,000 would be a slightly bearish signal.

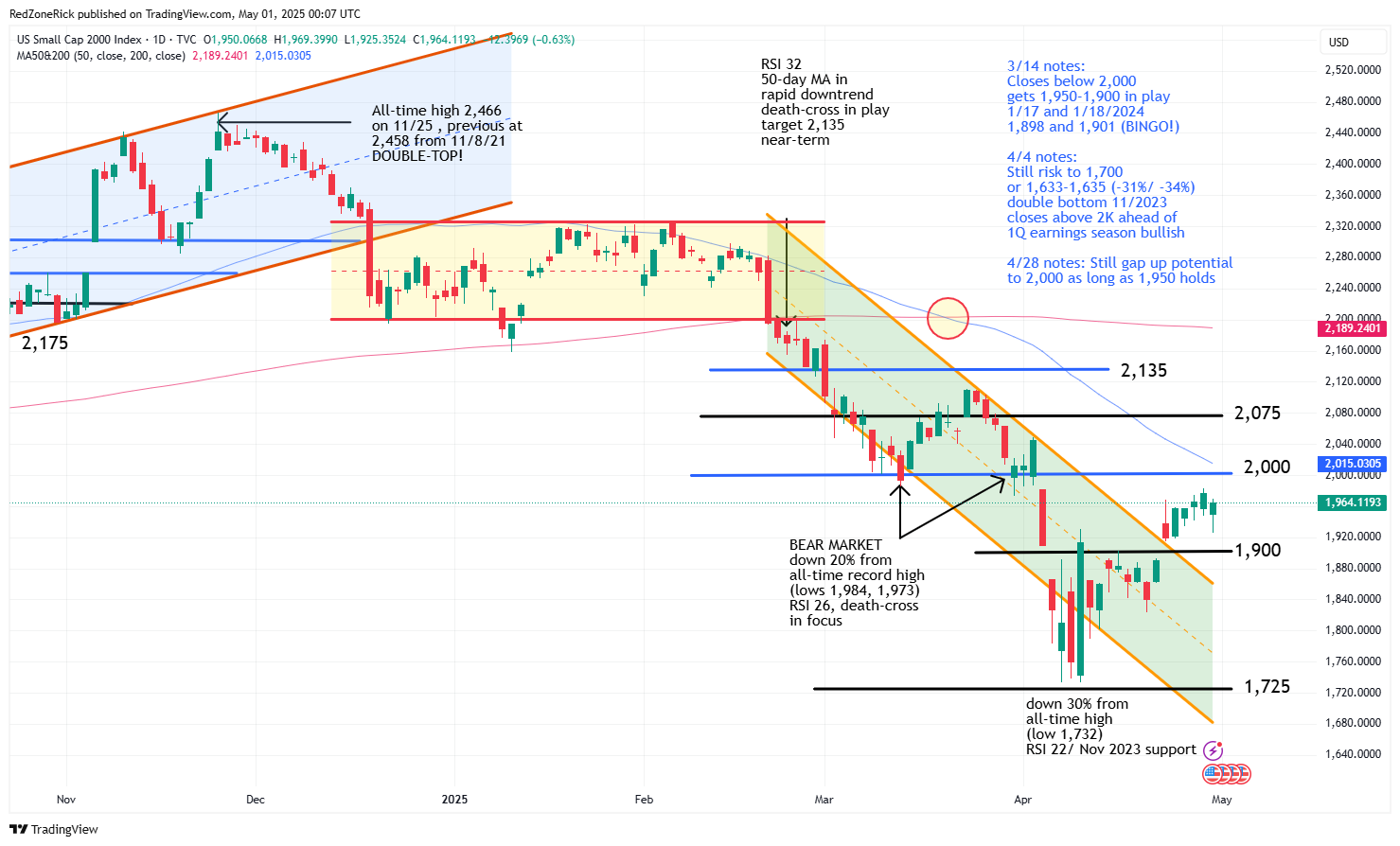

The Russell 2000 made a push to 1,982 on Tuesday but failed to make a higher high on Wednesday. Key resistance at 2,000 easily held with more important hurdles at 2,025 and the 50-day moving average.

Shaky support is at 1,950 with yesterday’s low at 1,925. A close back below 1,900 would signal another possible top with additional risk to 1,875-1,850 and the top of the prior downtrend channel.

The Nasdaq made higher highs to start the week with Tuesday’s peak at 17,500. Lower resistance at 17,500-17,750 was kissed and held. Closes above the latter and the 50-day moving average would be a more bullish development and suggest a possible near-term bottom.

Support is at 17,000-16,750 with Wednesday’s low at 16,959. A move below the latter would likely verify a false breakout with weakness to 16,500-16,250 and also the top of the prior downtrend channel.

The S&P made its seventh-straight higher high and has been holding key support and prior resistance at 5,500. The 50-day moving average is just north of 5,600 followed by 5,700-5,750 and the 200-day moving average.

A close below 5,400 and back into the previous downtrend channel would suggest a near-term peak.

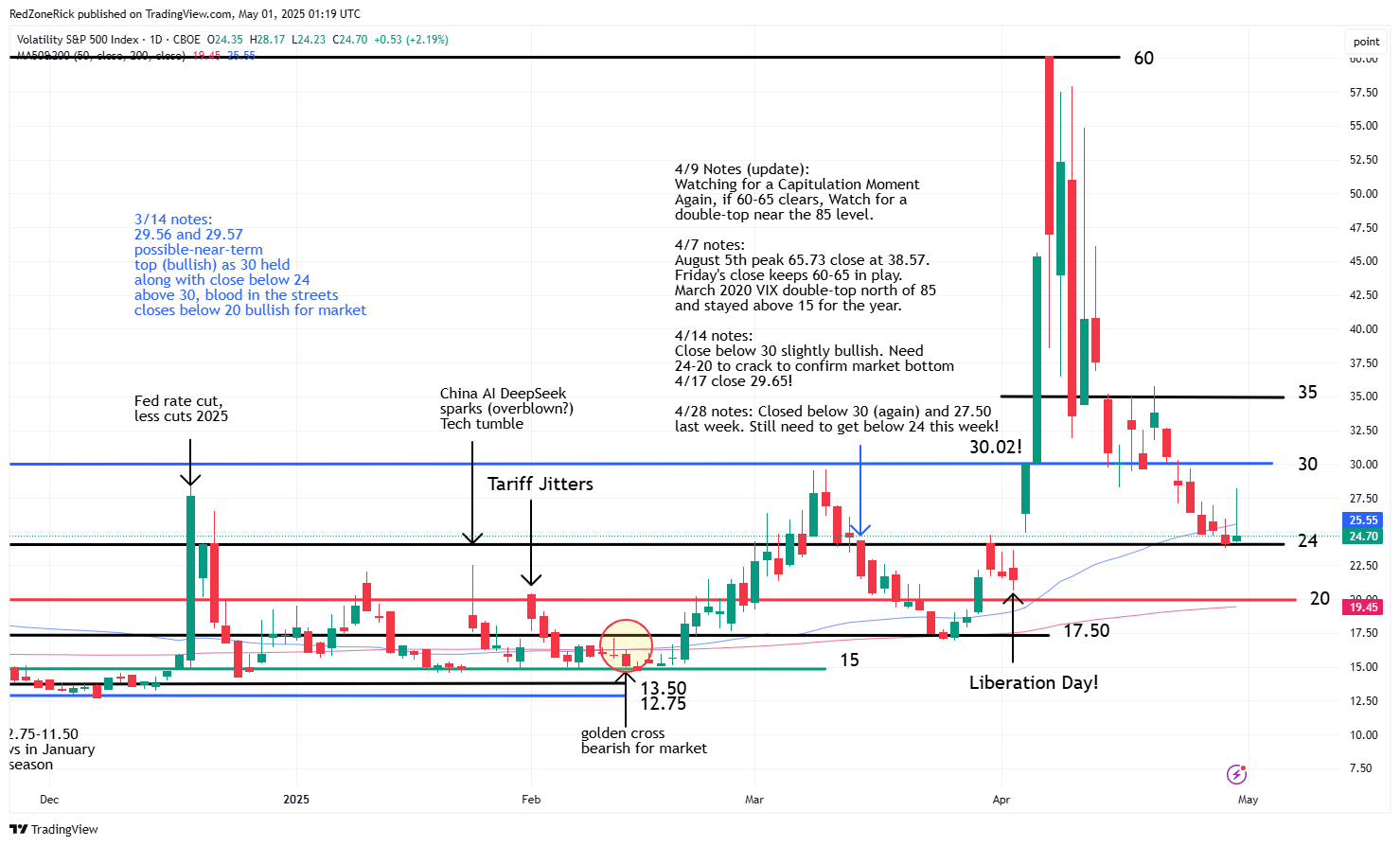

The Volatility Index (VIX) has closed below its 50-day moving average for three-straight sessions despite yesterday’s intraday spike to 28.17. A close back above 30 would be bearish for the market with stretch up to 35.

Support at 24 has basically been holding the past four sessions. Multiple closes below this level would be BULLISH for the market with additional weakness to 22.50-20.

After Wednesday’s close, a deal was announced between the United States and Ukraine over access to the country’s natural resources The new investment projects will help develop Ukraine’s natural resources including aluminum, graphite, oil and natural gas.

Also after Wednesday’s close, Microsoft (MSFT) and Meta Platforms (META) announced better-than-expected earnings. Shares of both companies were up 7% and 5%, respectively, and should provide a lift to Thursday’s open.