Options Trading: Is This the Ideal Environment for Calendar Spreads?

Shutterstock.com/g/synthex

In my trading, I usually establish positions with directional bias through the purchase of puts or calls. This can provide the most leverage and biggest bang for your buck. That is assuming the move you precited happens in a relatively short time and in a pretty orderly fashion.

But as we discussed Monday, the market seems to be losing some momentum and trading has become more choppy. This means owning options can hurt you as time decay or theta weighs on their value — as you wait for the anticipated move.

But, we also noted the implied volatility is currently near 52-week lows and that’s good news. It creates a great environment for utilizing calendar spreads; it consists of a short call in a near month, combined with a long call at the same strike in a further out month for a net debit.

The position will benefit in several ways; the accelerated or faster rate of decay of the near-term options sold short, by establishing these calendars during low volatility environments will gain value if volatility was to rise as the vega of the longer dated option we own is greater. So, for instance, as we head into an earnings event, the stock might not be going anywhere leading up to the event, but highly likely the premiums in options will rise in value as investors position for or hedge against a possible big move following the earnings. And lastly, the value of the position will increase as the underlying stock prices move towards the strike price.

Below is a profit/loss graph of a typical calendar spread; note the max profit is realized at expiration (the yellow line) at the strike price — in this case, $76.

Calendars can also offer the flexibility to make adjustments, or sell several cycles of weekly options to further reduce the cost basis.

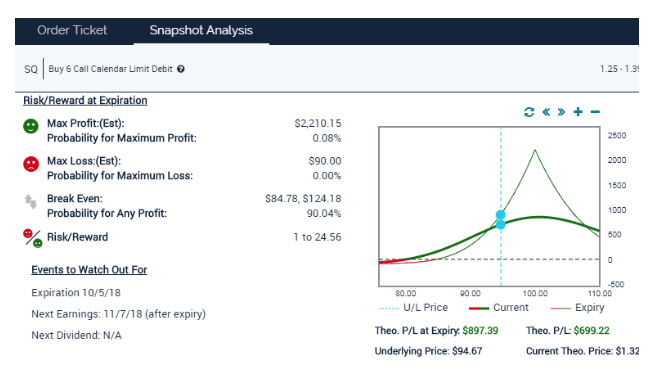

For example, in my Options350 service, we established a calendar in SQ on September 5th, by buying 6 contracts SQ October (10/19) 100 Calls and Selling to open 6 contracts SQ September (9/28) 100 Call For a net debit of $1.10.

Square shares have languished for a few weeks. But yesterday — when the stock jumped some 8% — we took advantage of the move and made an adjustment. Specifically, we bought to close the Sep(9/28) 100 calls and sold to open Oct (10/05) a $0.95 credit. This brings the cost basis down to a mere $0.15.

The risk graph of the position now looks like this: As you can see by reducing the cost basis

The post Options Trading: Is This the Ideal Environment for Calendar Spreads? appeared first on Option Sensei.