Options Trading: The Basics of Derivatives

Back at my old employer Minyanville I worked with John Succo to help put together this Introduction to Derivatives. I think it still stands a helpful basic overview of options trading. Here’s the first part:

We hear so much about derivatives, but the general public and even many professional traders aren’t quite sure what they are or how they impact our lives. Because leverage is almost always employed (only a fraction of the notional value is required for margin), the derivatives markets dwarf all other markets. The best estimate of the size of these markets is $150 trillion. By way of comparison the value of all U.S. equities listed on the NYSE is about $12 trillion. Because derivatives introduce a great deal of leverage into the financial system and the size of these markets is so great, regulators are very concerned about derivatives’ implications to the financial system.

The capital markets raise money for companies by selling what are termed cash securities, things that are familiar to most people like stocks and bonds. These are things people can buy or invest in and hold as assets to realize a return (although sometimes that return might be negative). There are also other hard assets like commodities and even real estate. These assets are all part of what is termed the “cash markets.” Currencies are a little different: they are loosely considered part of the cash markets, although not a hard asset (a currency is a vehicle of investment and saving that has value only relative to other currencies). Derivatives by their nature are based on cash markets.

The definition of derivative is “something obtained from a certain source.” A derivative then is a contract or agreement (this agreement almost always has a payoff and a time limit) whose value is based on the performance of a cash instrument (or more specifically its price movement). So a derivative contract basically says that if X happens to the price of the cash instrument over some specific period of time, one party will pay the other party Y. Common to all derivative contracts is an expiration date and leverage: In entering into the agreement, the parties are only required to post a fraction of the value of the eventual payoff.

In describing derivatives, I have broken the market into three basic product groups and written a primer on each:

1) Options

2) Futures

3) Structures (cash instruments with imbedded options)

There has been a great deal of academic discussion about the impact derivatives have made to the financial markets. In trading these markets over the years, there are two things I am certain of: Derivatives when used properly afford tremendous financial flexibility and because of the leverage they introduce, have caused a tremendous increase in overall volatility.

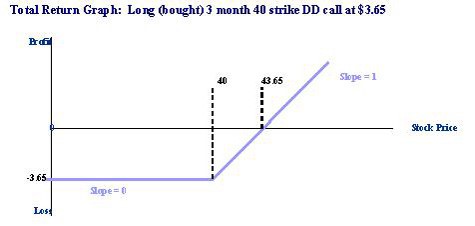

The most valuable aspect of an option is that it breaks apart the risk-return profile of the underlying stock. This creates the flexibility to buy for a price the upside or downside of a stock with leverage and limited risk, or sell for a price the upside or downside while incurring undefined risk. It also creates the ability to design more complex strategies around various stock prices. Graphs are a great tool in understanding options. Once you understood these graphs, you will be able to develop and analyze strategies using various combinations of options and stock around an expected stock return profile.

The buyer pays $3.65 per share per option or $365 for 100 shares (each option contract represents 100 shares). This is the maximum loss and occurs at any point below $40 per share. It is depicted as a zero slope line up to the strike price. Because the buyer has the right to buy the stock at $40 per share, any price above this will give the option an “intrinsic” value that increases dollar for dollar with the stock price. This is depicted by a line with a slope of 1.

The break-even stock price occurs at $43.65, where the intrinsic value equals the original cost. For every dollar that the stock goes up above this, the holder of the option makes $1 profit. As you can see, an option provides leverage: Instead of an investment of $40 x 100 shares or $4,000, a $365 investment makes an equivalent profit above a stock price of $43.65. As illustrated by the graph, the buyer of a call option is not only making the bet that the stock is going up, but that it will go up significantly and before the expiration date of the option. Time is against the buyer of the option.

Related: Are Buybacks Disguising a Weak Market?

Related: Are Buybacks Disguising a Weak Market?

The post Options Trading: The Basics of Derivatives appeared first on Option Sensei.